Uncategorized

PENSION TAX DEADLINE 2017 – 31st October & 14th November

Sep

Individuals who both pay and file their tax returns through the Revenue On-line Service (ROS) have until Tuesday 14th November 2017 to pay a pension contribution and elect to backdate the income tax relief against the 2016 tax year. Those who do not qualify for the ROS extension must do this by 31st October 2017. If you do not take this opportunity, you will not get another chance to reduce your 2016 income tax liability.

PENSION TAX DEADLINE FOR THE SELF-EMPLOYED

Backdating Income Tax Relief:

A self-employed person who wants to pay a personal pension or PRSA contribution and backdate the income tax relief against their 2016 earnings needs to do the following:

- Pay the contribution to the life office or PRSA provider on or before the return filing date; and

- Submit their tax return to Revenue on or before the return filing date.

The return filing date is 14th November 2017 for those who pay and file their returns using ROS. If there is any doubt about qualifying for the ROS extension we would recommend you pay your pension contributions and file your tax return by 31st October to ensure you meet the deadline.

Claiming Income Tax Relief on Personal pension or PRSA Contributions:

In order to claim income tax relief on contributions to a personal pension or PRSA the individual must be “chargeable to tax in respect of relevant earnings”. Relevant earnings refer to income of individuals who are:

Net relevant earnings are relevant earnings less charges in income (e.g. covenant payments, tax deductible maintenance payments, allowable interest) and losses or capital allowances related to the individual’s relevant earnings. Income which is not relevant earnings includes:

- Investment income (e.g. rental income);

- Sleeping partner;

- Earnings from an investment company where the client directly or in directly controls more than 20% or the company;

- Pension income (annuity income) or payments from Approved Retirement Fund (ARF) or Approved Minimum Retirement Fund (AMRF);

- Spouse’s income as you cannot take out a pension for your spouse’s income.

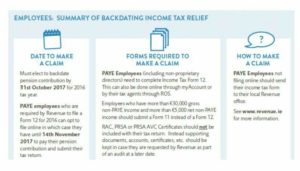

EMPLOYEES AVAILING OF THE TAX DEADLINE

Employees also have the opportunity to pay a pension contribution and set it against their 2016 tax bill. To claim income tax relief on their pension contribution, employees must pay their contribution to the appropriate pension contract for their circumstances.

- PRSA or Personal Pension: where the employee had Schedule E income during 2016 but was not a member of their employer’s company pension scheme.

- AVC or PRSA AVC: where the employee had Schedule E income during 2016, was a member of their employer’s company pension scheme during 2016 and is still in that same employment.

Once an employee leaves employment where they were a member of a company pension scheme, they cannot make any further pension contributions in respect of the income from that employment. Note: a termination payment made on leaving employment (under Section 123 TCA 1997) is not considered remuneration for pension purposes. This would include termination payments on redundancy, payment in lieu of notice and other ex-gratia payments. However, part or all of such a termination payment may qualify for tax relief under other available exemptions.

Backdating Income Tax Relief:

An employee has until 31st October 2017 to:

- Pay their pension contribution to the appropriate pension contract (see above); and

- Send their tax return to Revenue, electing to backdate the pension contribution to 2016 tax year.

Where an employee elects to backdate a contribution to a previous tax year they need to ensure that relief has not already been given in the current tax year. Where the contribution is paid through payroll under the net pay arrangement income tax relief is automatic and is given in the current tax year.

Late Returns:

Revenue will not permit tax relief to be backdated against 2016 if you have not elected to claim the tax relief in that tax year as part of your tax return, or if a tax return has not been filed on time. This applies even if the pension contribution was paid by 31st October 2017.

Revenue has made an exception for PAYE employees who are not normally self-assessed where they:

- Pay a contribution by 31st October 2017; and

- Retire in the year in which the contribution was made, i.e. retire in 2017; and

- File a return and elect to backdate the contribution on or before the 31st December 2017.

If the above conditions are met then income tax relief against 2016 can be claimed.

If a person is not eligible for tax relief for any reason, this is not grounds for a refund of contributions. If tax relief cannot be claimed currently, then the person may be able to carry the relief forward and claim relief against relevant earnings in the future.

EARNINGS LIMIT AND INDIVIDUALS WITH DUAL INCOMES

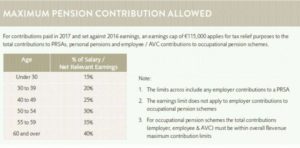

Tax relief on pension contributions are subject to two limits:

- The age related percentage of salary as shown above;

- The earnings limit which is set at €115,000 for the 2016 and 2017 tax years.

Where someone has two sources of earnings, one from an office of employment where they are a member of a contributory occupational pension scheme (pensionable employment) and the other either non-pensionable or from self-employment, the pensionable earnings uses up the earnings limit first.

EXAMPLE 1 – Pensionable earnings greater than the €115,000 earnings limit.

- John, age 45

- Employment Income: €150,000

- Pension Employee Contribution 5%: €7,500

- Self-Employed Income: €45,000

Based on John’s age the maximum contribution he can make to the occupational pension scheme and claim tax relief is 25% of his earnings, capped at €115,000. So John’s maximum pension contribution is 25% x €115,000 = €28,750. As he is already contributing €7,500 he has scope to pay AVCs of up to €21,250. John’s pensionable income uses up the earnings limit first and as that income is greater than the earnings limit he cannot claim tax relief against any personal pension or PRSA contributions made in respect of his self-employed earnings. This applies even if he does not maximise his AVCs to the company pension scheme.

EXAMPLE 2 – Total income over the €115,000 earnings limit.

- Kate, age 45

- Employment Income: €80,000

- Pension Employee Contribution 5%: €4,000

- Self-Employed Income: €55,000

Based on his age the maximum contribution Kate can make to the occupational pension scheme and claim tax relief is 25% of his salary i.e. 25% x €80,000 = €20,000. She is already paying employee contributions of €4,000 so she has scope to make further AVCs of €16,000. Kate’s pensionable employment uses up the earnings limit first, so she can only make pension contributions against €35,000 of her self-employed earnings i.e. €115,000 – €80,000 = €35,000. So the maximum pension contribution she can pay and claim tax relief on against her self-employed earnings is 25% x €35,000 = €8,750. This applies even if she does not maximise her AVCs to the company pension scheme.

EXAMPLE 3 – Total income less than €115,000 earnings limit.

- Mike, age 52

- Employment Income: €30,000

- Pension Employee Contribution 5%: €1,500

- Self-Employed Income: €60,000

Based on Mike’s age the maximum he can contribute to the company pension scheme and claim income tax relief is 30% of salary i.e. 30% x €30,000 = €9,000. He is already paying an employee contribution of €1,500 so has scope to make AVCs of up to €7,500. As his total earnings are less than €115,000, the earnings limit has no impact on the personal pension or PRSA contribution he can pay against his self-employed earnings, which based on age would be 30% x€60,000 = €18,000.