Financial Services

How To Know When To Get Out Of The Market

Feb

- Please see below a great article by Tim Maurer on the trade-offs investors face when choosing to stay invested in time of market turbulence.

Has the market’s recent volatility worried you? Me too. It’s inevitable. Apparently, it’s how we’re wired. But better understanding that wiring can give us a clear decision-making framework to help us know if and when to get out of the market.

The field of behavioural finance has demonstrated that the pain we derive from market losses impacts us twice as much as the pleasure we feel from market gains. For this reason, investors are well served to name and address these emotions instead of setting them aside as they (unfortunately) have been taught.

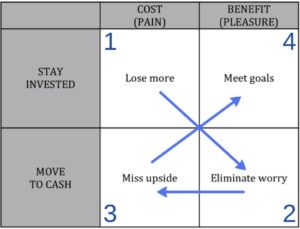

We’ve all heard of the cost/benefit decision-making model, but “cost” and “benefit” are intellectual constructs too distant from the actual emotions that drive our decision-making. We need to address the gut—the “pain” and the “pleasure” associated with a tough decision. The following four-step model seeks to merge the head and the gut. And while it’s applicable in virtually any either/or scenario, let’s specifically address the decision to stay invested in the market or to move to cash:

1) The pain of staying invested is that I could lose even more. This is an entirely realistic possibility. What’s more, the pain is compounded when subsequent headlines—or your investment account statements—goad you into thinking that you could’ve—should’ve—avoided this pain if only you’d gotten out sooner. When this realization strikes the broader investing collective, it’s called capitulation—the moment investors give up en masse—and it typically signals the beginning of the forthcoming recovery, even the next bull market.

2) The pleasure of moving to cash is that my worry is eliminated and I’m guaranteed not to lose any more. Undeniably, you’ll sleep better tonight. But.

3) The pain involved in moving to cash is that I may miss the upside, thereby eliminating my opportunity to recoup recent losses in the next market up move. We know this, but the recent pain of loss is a far more powerful emotion than the projected pleasure, however probable, of gains in the future. The pain in box number three is often dampened by the hope that you’ll be able to get back into the market on the way up, a gamble statistically proven to be in the neighborhood of hopeless.

4) The pleasure in staying invested is that I’m giving myself a better chance to achieve my financial goals in the long term—the whole reason I invested in market in the first place. The market historically has paid investors a premium over cash and bonds precisely because it requires you to endure times of volatility. Without volatility, we’d have no reason to expect higher long-term gains. And for most of us, without the higher long-term gains we expect from equities, we simply wouldn’t meet our financial goals.

Does this imply there is never a reason to sell your market positions following a decline? No. The above framework assumes that your portfolio is diversified. It also assumes your portfolio is appropriately balanced with the stabilizing force of conservative fixed income allocated according to your ability (time horizon) and willingness (intestinal fortitude) to take risk. If this is not the case, there may, indeed, be grounds for change.

For the sake of creating a clear illustration, this framework only address the two extreme options of “sticking with the plan” or bailing out. Of course, there is a vast middle, and if you find that a typical correction or frightening headline has provided real-time evidence that your risk tolerance is not as high as you previously thought, recalibrating your portfolio may be entirely appropriate. It is imperative, however, to remember that the degree to which you shift out of riskier assets and into more secure assets will send you back to box number three. You’ll have to consider how much lost ground you’ll be able to reclaim in the likely subsequent market advance.

Please don’t paint me as an unrepentant stock market cheerleader. I believe that most investors—and even, perhaps especially, financial advisors—don’t fully appreciate and consider the serious emotions associated with volatility in investing. For this reason, I believe most people default to portfolios that are likely too heavily tilted toward stocks. Furthermore, if you don’t need the expected higher returns of the stock market in order to reach your financial goals, I’m inclined to recommend surprisingly low allocations to market exposure. On more than one occasion, I’ve recommended portfolios with absolutely no equities [gasp] for clients who didn’t need the excess returns and clearly didn’t have the stomach for volatility.

But if you’re already in the market, and in a well-conceived portfolio, the decision to get out is one deserving careful consideration, employing both the heart and the mind.

Source: “How to know when to get out of the market” by Tim Maurer